REGISTRO DOI: 10.69849/revistaft/ma10202601100849

Aline Caroline Moraes Oliveira

Abstract

This article examines how fixed-income markets and investors react to changes in benchmark interest rates and credit risk conditions. Using evidence from empirical research on sovereign bonds, corporate credit, and private-credit markets, it explains how rising or falling interest-rate cycles affect duration decisions, cross-asset allocation, and the relative attractiveness of fixed income versus equities. It also evaluates whether credit spreads adequately compensate investors for expected default losses, liquidity premia, and systematic risk across different rating categories. Findings show that credit-risk pricing is cyclical, market spreads often lead rating actions, and structural differences between sovereign bonds, corporate issuances, and private-credit instruments shape investor behaviour.

Keywords: Fixed-income markets; interest rates; credit spreads; credit risk; debentures; sovereign bonds; private credit; CRI/CRA; duration management; investor behaviour.

The fixed-income market responds to changes in benchmark interest rates and credit risk through both mechanical pricing adjustments and shifts in investor behaviour. When interest rates rise, existing bond prices fall due to higher discount rates, leading investors to shorten duration, move toward floating-rate instruments, or increase allocations to higher-yield private credit. Conversely, falling rates raise the market value of long-duration bonds and diminish the relative appeal of cash-like instruments. Empirical evidence shows that these cross-asset reallocations are systematic, as higher rates reduce the attractiveness of long-duration equity exposures while improving real yields in government securities (Zaremba et al., 2023).

Public sovereign bonds, investment-grade corporate bonds, speculative corporate bonds, and private-credit instruments such as debentures and real-estate receivable securities (e.g., CRI/CRA in Brazil) differ substantially in terms of return, liquidity, and credit risk. Sovereign bonds typically offer the lowest credit risk and highest liquidity, serving as the risk-free benchmark. Corporate and private-credit instruments compensate investors with higher yields for assuming expected default losses, liquidity frictions, and structural risks. These premia vary with macroeconomic cycles: during rising-rate environments, new issuances price higher coupons, while secondary-market prices of low-coupon bonds fall, prompting active duration management (Fernandes, 2014).

A central question for investors is whether credit spreads adequately compensate for credit risk across rating categories. Studies show that only part of the spread reflects expected default losses, while substantial portions arise from liquidity premia and compensation for systematic credit risk (Berndt et al., 2018). During stable economic periods, spreads compress and may fail to price tail risks adequately; during stress periods, spreads widen sharply and often overshoot fundamental deterioration, creating temporary excess-risk premia (European Central Bank, 2016).

Credit spreads often lead rating-agency actions. Bonds that trade at significantly wider spreads than peers of similar rating tend to face higher probabilities of future downgrades and worse subsequent performance, indicating that market-implied credit risk is more responsive than agency ratings. This effect is amplified in private-credit markets, where information asymmetry is greater and liquidity scarcer (Dai, 2024). Effective credit monitoring therefore requires integrating spread analysis, liquidity assessment, covenant quality, and issuer fundamentals.

From an allocation standpoint, monetary policy cycles alter investor incentives and capital flows. In tightening cycles, duration risk becomes more punitive and investors favour short-term or floating-rate exposures, while rising policy rates increase issuer funding costs. In easing cycles, declining short-term yields encourage investors to extend duration or assume greater credit risk to maintain returns, compressing spreads and raising future vulnerability. These dynamics are especially relevant in emerging markets, where private credit—such as Brazilian debentures and CRI/CRA—often offers elevated yields that must be weighed against liquidity, collateral structure, and recovery prospects (Fernandes, 2014).

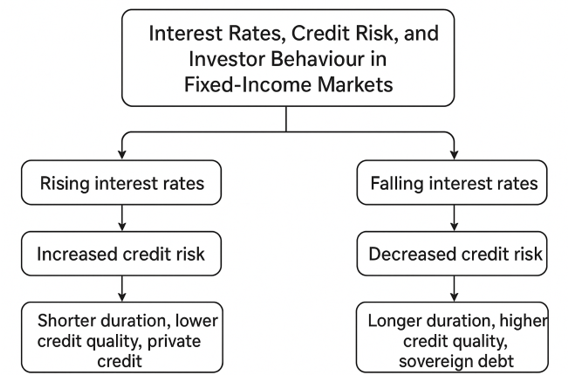

The flowchart illustrates how shifts in monetary policy and credit conditions jointly influence investor behavior in fixed-income markets. When interest rates rise, credit risk tends to increase as borrowing costs climb and issuer fundamentals weaken, leading investors to shorten duration, reduce exposure to higher-quality long-duration assets, and move toward private credit or shorter-term instruments that better compensate for risk. In contrast, falling interest rates typically reduce credit risk, strengthen issuers’ balance sheets, and enhance the attractiveness of longer-duration and higher-quality bonds, including sovereign debt. Together, these dynamics show how changes in the interest-rate cycle shape credit spreads, risk premia, and portfolio allocation decisions.

Figure 1. Investor Reactions to Interest Rate and Credit Risk Dynamics in Fixed-Income Markets.

Source: Created by author.

In conclusion, interest-rate movements and credit-risk dynamics jointly shape the valuation and attractiveness of fixed-income assets. While higher nominal yields enhance the appeal of fixed income, the core investment decision depends on whether incremental yield properly compensates for duration, liquidity, and default risks. Empirical evidence shows that credit spreads embed both fundamental default expectations and time-varying risk premia. Investors benefit from combining macroeconomic regime analysis with granular credit underwriting to navigate sovereign, corporate, and private-credit instruments within the broader context of market cycles.

References

Berndt, A., Duffie, D., & Zhu, Y. (2018). Corporate Credit Risk Premia. National Bureau of Economic Research, Working Paper No. 24213.

Dai, H. (2024). Corporate credit risk and bond yield spreads. Journal of Fixed Income.

European Central Bank (ECB). (2016). Credit Spreads, Economic Activity and Fragmentation. ECB Working Paper No. 1930.

Fernandes, M. (2014). Brazilian corporate debt issuance: structure and dynamics. Revista Brasileira de Economia.

Zaremba, A., Kizys, R., & Karathanasopoulos, A. (2023). Interest rate changes and the cross-section of global equity returns. International Review of Financial Analysis.

SANTOS,Hugo;PESSOA,EliomarGotardi.Impactsofdigitalizationontheefficiencyandqualityofpublicservices:Acomprehensiveanalysis.LUMENETVIRTUS,[S.l.],v.15,n.40,p.44094414,2024.DOI:10.56238/levv15n40024.Disponívelem:https://periodicos.newsciencepubl.com/LEV/article/view/452.Acessoem:25jan.2025.

Filho, W. L. R. (2025). The Role of Zero Trust Architecture in Modern Cybersecurity: Integration with IAM and Emerging Technologies. Brazilian Journal of Development, 11(1), e76836. https://doi.org/10.34117/bjdv11n1-060

Oliveira, C. E. C. de. (2025). Gentrification, urban revitalization, and social equity: challenges and solutions. Brazilian Journal of Development, 11(2), e77293. https://doi.org/10.34117/bjdv11n2-010

Pessoa, E. G. (2024). Pavimentos permeáveis uma solução sustentável. Revista Sistemática, 14(3), 594–599. https://doi.org/10.56238/rcsv14n3-012

Filho, W. L. R. (2025). THE ROLE OF AI IN ENHANCING IDENTITY AND ACCESS MANAGEMENT SYSTEMS. International Seven Journal of Multidisciplinary, 1(2). https://doi.org/10.56238/isevmjv1n2-011

Antonio, S. L. (2025). Technological innovations and geomechanical challenges in Midland Basin Drilling. Brazilian Journal of Development, 11(3), e78097. https://doi.org/10.34117/bjdv11n3-005

Pessoa, E. G. (2024). Pavimentos permeáveis uma solução sustentável. Revista Sistemática, 14(3), 594–599. https://doi.org/10.56238/rcsv14n3-012

Pessoa, E. G. (2024). Pavimentos permeáveis uma solução sustentável. Revista Sistemática, 14(3), 594–599. https://doi.org/10.56238/rcsv14n3-012

Eliomar Gotardi Pessoa, & Coautora: Glaucia Brandão Freitas. (2022). ANÁLISE DE CUSTO DE PAVIMENTOS PERMEÁVEIS EM BLOCO DE CONCRETO UTILIZANDO BIM (BUILDING INFORMATION MODELING). Revistaft, 26(111), 86. https://doi.org/10.5281/zenodo.10022486

Eliomar Gotardi Pessoa, Gabriel Seixas Pinto Azevedo Benittez, Nathalia Pizzol de Oliveira, & Vitor Borges Ferreira Leite. (2022). ANÁLISE COMPARATIVA ENTRE RESULTADOS EXPERIMENTAIS E TEÓRICOS DE UMA ESTACA COM CARGA HORIZONTAL APLICADA NO TOPO. Revistaft, 27(119), 67. https://doi.org/10.5281/zenodo.7626667

Eliomar Gotardi Pessoa, & Coautora: Glaucia Brandão Freitas. (2022). ANÁLISE COMPARATIVA ENTRE RESULTADOS TEÓRICOS DA DEFLEXÃO DE UMA LAJE PLANA COM CARGA DISTRIBUÍDA PELO MÉTODO DE EQUAÇÃO DE DIFERENCIAL DE LAGRANGE POR SÉRIE DE FOURIER DUPLA E MODELAGEM NUMÉRICA PELO SOFTWARE SAP2000. Revistaft, 26(111), 43. https://doi.org/10.5281/zenodo.10019943

Pessoa, E. G. (2025). Optimizing helical pile foundations: a comprehensive study on displaced soil volume and group behavior. Brazilian Journal of Development, 11(4), e79278. https://doi.org/10.34117/bjdv11n4-047

Pessoa, E. G. (2025). Utilizing recycled construction and demolition waste in permeable pavements for sustainable urban infrastructure. Brazilian Journal of Development, 11(4), e79277. https://doi.org/10.34117/bjdv11n4-046

Testoni, F. O. (2025). Niche accounting firms and the Brazilian immigrant community in the U.S.: a study of cultural specialization and inclusive growth. Brazilian Journal of Development, 11(5), e79627. https://doi.org/10.34117/bjdv11n5-034

Silva, J. F. (2025). Desafios e barreiras jurídicas para o acesso à inclusão de crianças autistas em ambientes educacionais e comerciais. Brazilian Journal of Development, 11(5), e79489. https://doi.org/10.34117/bjdv11n5-011

Silva, E. N. da. (2025). Urban circular microfactories: local micro-plants for regenerative urban economies. Brazilian Journal of Development, 11(9), e82335. https://doi.org/10.34117/bjdv11n9-059

DA SILVA, Eduardo Nunes. GREEN NANOTECHNOLOGY APPLIED TO CIRCULAR MANUFACTURING. LUMEN ET VIRTUS, [S. l.], v. 14, n. 32, 2024. DOI: 10.56238/levv14n32-029. Disponível em: https://periodicos.newsciencepubl.com/LEV/article/view/AEW09. Acesso em: 4 nov. 2025.

Recycling of Rare Earth Elements Using Ionic Liquids for Regenerative Manufacturing. (2023). International Seven Journal of Multidisciplinary, 2(5). https://doi.org/10.56238/isevmjv2n5-037